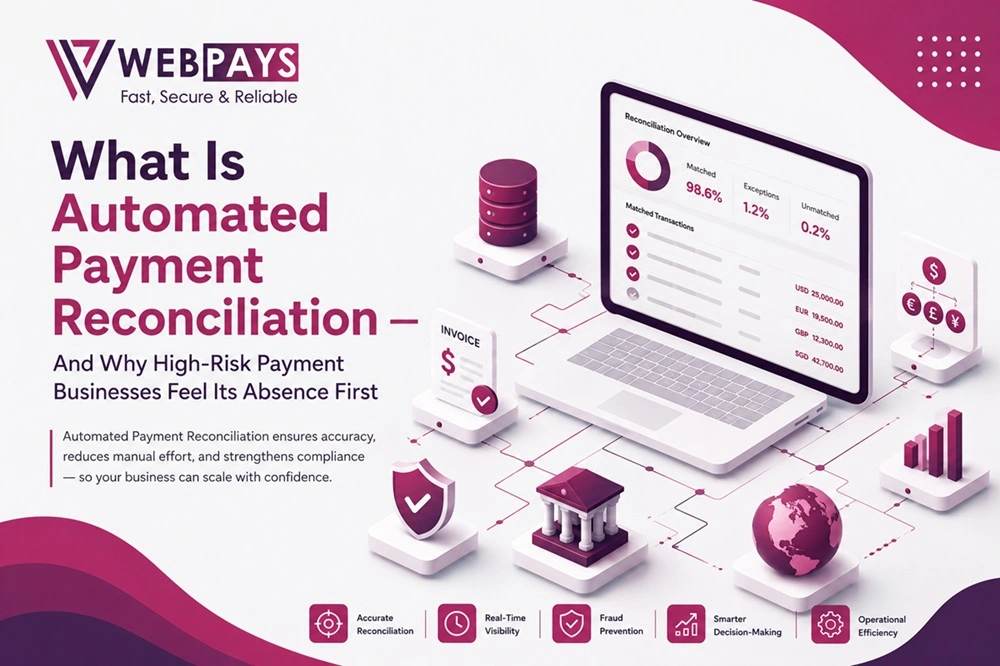

Automated payment reconciliation is the process of confirming that what a payment gateway says happened to a transaction actually matches what happened to the money — across the acquirer settlement file, the fees deducted, any refund or chargeback applied, and the amount that lands in a merchant payout — without a finance team manually checking each transaction by hand.

Every payment business eventually needs this. High-risk payment businesses need it first, because the gap between “authorized” and “actually settled, net of every deduction” is simply wider in this segment. Rolling reserves hold back a percentage of every transaction for months. Chargeback rates run several multiples higher than standard retail. Multiple acquirers are the norm, not the exception, because single-acquirer setups rarely survive at high-risk volume. Each of those factors is a place where the gateways transaction record and the acquirer actual settlement can quietly diverge — and reconciliation is the only process built to catch that divergence before it becomes a finance problem or a merchant dispute.

Why Reconciliation Breaks Down Fastest for High-Risk PSPs and Global Payment Businesses

A single-acquirer, single-currency payment business can run reconciliation in a spreadsheet for a surprisingly long time before it becomes painful. Add a second acquirer and that changes immediately — not because the volume doubled, but because now there are two settlement file formats, two fee schedules, two reserve policies, and potentially two different definitions of “settled” to reconcile against a single internal transaction record.

High-risk payment businesses hit this wall early because multi-acquirer routing is often a day-one requirement, not a growth-stage upgrade — a single acquirer relationship rarely provides enough approval-rate stability or enough risk tolerance to run a full high-risk book alone. Layer in multi-currency settlement, cross-border merchants, and chargeback windows that can stretch 60-120 days past the original transaction date, and the honest answer is that manual reconciliation isn’t a slower version of the same process — past a certain point, it stops being able to do the job at all. Mismatches don’t get caught; they get absorbed as “shrinkage” that nobody can fully explain.

How Automated Payment Reconciliation Actually Works, Step by Step

Strip away the vendor language and reconciliation is really five things happening in sequence, continuously, rather than in a monthly batch:

- Pulling in every relevant record — the gateway own transaction log, the acquirer settlement file, the acquiring banks deposit record, and any refund or chargeback notice — as each one becomes available, not waiting for all of them to arrive.

- Standardizing formats. Every acquirer reports differently: different field names, different date formats, different status vocabulary for the same event. This step translates all of it into one internal structure before anything gets compared.

- Matching each transaction across systems using shared identifiers — transaction ID, acquirer reference number, amount, and timestamp — to confirm the gateway record and the acquirer record describe the same event.

- Breaking down every deduction separately — interchange, scheme fees, gateway fees, FX conversion spread, reserve holdback — so the net amount is explainable line by line, not just a smaller number than expected.

- Routing anything that doesn’t match cleanly into an exception queue, tagged with why it failed to match, so a human only looks at the small percentage of transactions that actually need a decision.

The output isn’t a report. It is a live, per-transaction status — authorized, captured, settled, partially settled, refunded, disputed, or held in reserve — that both the payment business and its merchants can trust without cross-checking it manually.

What Payment Data Actually Needs to Be Reconciled — Not Just Matched

Matching two transaction IDs together is the easy part. The data that actually needs reconciling — meaning explained, not just confirmed — is everything that can change the amount between authorization and final payout:

- Authorization vs. capture status, since an authorized amount and a captured amount aren’t guaranteed to be identical, particularly on partial fulfillments.

- Gross settlement amount versus net settlement amount, with every deduction between the two itemized rather than bundled.

- FX rate applied at settlement, when the transaction currency and settlement currency differ — this is one of the most common sources of “the numbers don’t match” confusion in global operations.

- Refund and chargeback events, which frequently post days or weeks after the original transaction and need to be traced back to it, not treated as standalone line items.

- Rolling reserve movement — both the amount withheld on a given transaction and the amount released from reserve on a prior one.

- Merchant-level allocation, for any PSP settling on behalf of multiple merchants — every fee, refund, and reserve adjustment has to land against the correct merchant, not just the correct acquirer.

Miss any one of these and the reconciliation isn’t wrong, exactly — it just incomplete in a way that only shows up later, usually as a merchant asking why their payout doesn’t match their own records.

Manual vs. Automated Reconciliation: What Changes at High-Risk Volume

The honest comparison isn’t “manual is slower.” It’s that manual reconciliation is a sampling process disguised as a complete one — a finance team checks the transactions that look unusual and assumes the rest matched, because checking all of them by hand isn’t possible past a few hundred transactions a day.

Automated reconciliation checks all of them, every time, and only surfaces the ones that genuinely need a human decision. That shift matters most in exactly the conditions high-risk payment businesses operate under: multiple acquirers, multi-currency settlement, and a chargeback timeline long enough that the “unusual” transaction a manual process would have flagged already settled and closed the book weeks before the dispute arrived.

Why Reconciliation Has to Be Built Into the Gateway, Not Bolted On Afterward

Reconciliation software that sits outside the payment gateway is working from a copy of the data, not the source of it — someone still has to export transaction records, upload settlement files, and keep the two systems in sync manually, which reintroduces exactly the manual bottleneck reconciliation is supposed to remove.

When reconciliation runs inside the gateway itself, it has direct access to the transaction record the moment it’s created, the routing decision that was made, and the acquirer response as it comes back — no export step, no separate system to keep updated, no lag between something happening and it being reconciled. For a high-risk payment business, this also means reconciliation data can feed back into routing decisions in the other direction: if one acquirer’s settlement data is consistently showing higher fee deductions than quoted, that’s a routing input, not just a finance footnote.

The Reconciliation Challenges That Are Unique to Global, High-Risk Payment Operations

Reconciling Across Multiple Providers and Acquirers

Every acquirer has its own settlement file structure, its own status vocabulary, and its own timing — some settle daily, some weekly, some batch differently by card network. None of that is standardized industry-wide, so the reconciliation layer has to do the translation work that the acquirers themselves won’t.

Making Sense of Multi-Currency Settlements

A transaction taken in one currency and settled in another introduces an FX rate the merchant never sees at checkout, plus a conversion spread that varies by acquirer and by day. Without tracking the exact rate applied at settlement, “the numbers don’t add up” becomes a recurring, unresolved complaint rather than a five-minute explanation.

Tracking Refunds and Chargebacks Without Losing the Thread

A chargeback filed 90 days after a transaction has to be traced back to that original transaction, the acquirer it ran through, and the merchant it belongs to — and it has to adjust that merchant balance correctly even though the original settlement closed out long ago. Treated as a standalone event instead of a follow-on to the original transaction, chargebacks are one of the fastest ways for merchant balances to quietly drift from reality.

Untangling Fee Complexity Across Providers

Interchange, scheme fees, acquirer markup, gateway fees, chargeback fees, and reserve holdback can all apply to the same transaction, and no two acquirers itemize them identically. Without separating each deduction individually, “net revenue” becomes a number nobody can fully defend if a merchant — or an auditor — asks how it was calculated.

Getting Merchant-Level Accounting Right at Scale

A PSP settling for dozens or hundreds of merchants has to route every fee, refund, and reserve adjustment to the correct merchant ledger, not just the correct acquirer total. This is where spreadsheet-based reconciliation fails first, because merchant-level allocation logic gets more complex with every merchant added, not linearly but compoundingly.

Catching Delayed or Missing Settlements Before They Become Disputes

A settlement that’s late — because of a banking holiday, a risk hold, or a provider-side delay — looks identical to a settlement that’s simply missing until someone checks. Automated exception flagging catches the gap within a day or two; a monthly manual review catches it after a merchant has already noticed their payout didn’t arrive and escalated.

Build In-House or Use White-Label Reconciliation Software? The Real Trade-Offs

Building reconciliation in-house gives full control over matching logic and merchant-ledger structure, but it also means owning every future acquirer integration, every format change an acquirer makes without notice, and every compliance requirement that touches financial reporting — indefinitely, as a permanent engineering commitment rather than a one-time build.

Reconciliation delivered as part of a white-label gateway infrastructure trades some of that control for speed and for the fact that reconciliation logic sits directly on the transaction data instead of a synced copy of it. For most PSPs and global payment businesses, the deciding factor isn’t whether in-house control would be nice — it usually would be — it’s whether maintaining that control indefinitely is a better use of engineering capacity than the core product itself.

What to Actually Look for in Automated Reconciliation Functionality

Not all “automated reconciliation” claims mean the same thing. The functionality that actually matters for a high-risk, multi-acquirer operation includes:

- True multi-acquirer normalization, not just support for one additional provider bolted onto a single-acquirer design.

- Itemized fee breakdown per transaction, not a blended net figure.

- Merchant-level ledger allocation, if the business settles on behalf of other merchants.

- Exception queues with a reason code attached — “unmatched” isn’t useful without knowing why.

- Chargeback and refund linkage back to the original transaction, regardless of how much time has passed.

- Reserve tracking that shows both withheld and released amounts as separate, auditable events.

If a reconciliation feature can’t answer “why doesn’t this net amount match the gross amount,” it’s a matching tool, not a reconciliation one — the two get marketed interchangeably far more often than they should be.

How Automated Reconciliation Changes What a PSP’s Operations Team Can Do

The practical shift isn’t just fewer hours spent on spreadsheets, though that’s real. It’s that operations and finance teams stop reacting to reconciliation problems after a merchant notices them and start catching mismatches while they’re still a same-day exception instead of a two-month-old dispute. That changes the nature of merchant conversations — from “let us look into that and get back to you” to being able to explain a discrepancy on the same call it’s raised. For a high-risk PSP, where merchant trust is already harder-won than in standard commerce, that difference compounds.

Where WebPays Automated Payment Reconciliation Fits Into a High-Risk Gateway Stack

Reconciliation is only as good as its proximity to the actual transaction and routing data — a bolted-on tool working from exported files is always reconciling yesterday’s picture. Because WebPays’ reconciliation runs inside the same infrastructure that handles routing, cascading, and multi-acquirer settlement for high-risk merchants, it has direct access to the transaction record from the moment it’s created through final payout, across every connected acquirer and currency — no separate export or sync step in between. For PSPs and global payment businesses built specifically around high-risk categories, that means merchant-level balances, fee breakdowns, and exception flags reflect the same data the routing engine is already using, rather than a second, delayed copy of it.

Reconciliation Mistakes That Quietly Cost High-Risk PSPs Money and Trust

- Treating reconciliation as a monthly finance task rather than a continuous, per-transaction process — by the time a monthly review catches a mismatch, the chargeback window on it may already be closing.

- Reconciling at the acquirer level only, without allocating fees and adjustments down to the individual merchant, which makes merchant-facing reports unreliable even when the top-line numbers are correct.

- Using inconsistent transaction identifiers across the gateway, acquirer, and internal systems, which breaks automated matching and pushes far more transactions into manual review than should be necessary.

- Bundling all fees into one blended deduction instead of itemizing interchange, scheme fees, and gateway costs separately, which makes it impossible to answer a merchant’s or auditor’s question about where the money went.

- Not linking refunds and chargebacks back to original transactions, which lets merchant balances drift from reality without an obvious trigger.

- Choosing gateway infrastructure without evaluating its reconciliation and reporting layer, then discovering the gap only after merchant volume has already scaled past what a workaround can handle.

Reconciliation Is the Financial Truth Layer Behind Every High-Risk Payment Business

Routing and fraud tooling decide whether a transaction gets approved. Reconciliation decides whether anyone can actually trust the resulting numbers — what settled, what it cost, what a merchant is owed, and why. For a high-risk payment business running multiple acquirers across multiple currencies, that layer isn’t a finance department convenience. It’s the difference between catching a settlement problem in a day and finding out about it from an angry merchant two months later.

FAQ

What is automated payment reconciliation?

Automated payment reconciliation is software-driven matching of transaction, settlement, fee, refund, chargeback, and payout data across a payment gateway, acquirers, and merchant accounts, so discrepancies are flagged automatically instead of requiring a finance team to check every transaction by hand.

Why do high-risk PSPs and global payment businesses need automated reconciliation?

High-risk PSPs typically run multiple acquirers, multi-currency settlement, elevated chargeback rates, and rolling reserves — all of which create more places for a transaction record and its actual settlement to diverge than standard-risk merchants encounter, making manual reconciliation unreliable past a fairly small volume.

How does automated reconciliation work inside a payment gateway?

It continuously pulls in transaction, settlement, and dispute data as it arrives, standardizes each acquirer’s format into one structure, matches records using shared identifiers, itemizes every fee and deduction, and routes anything that doesn’t match cleanly into an exception queue for review.

Is reconciliation included in white-label payment gateway software, or is it separate?

It varies by provider. Reconciliation delivered inside the gateway infrastructure has direct access to transaction and routing data as it’s created; reconciliation sold as a separate tool typically works from exported or synced data, which introduces delay and an extra system to maintain.

What’s the difference between payment reconciliation and settlement reporting?

Settlement reporting shows the amount an acquirer deposited. Reconciliation goes further, matching that deposit against the original transactions, fees, refunds, chargebacks, and reserve movements that produced it, so the net figure is explainable rather than just observed.

How can WebPays help with automated payment reconciliation?

WebPays runs reconciliation inside the same infrastructure that handles routing and multi-acquirer settlement for high-risk merchants, giving PSPs and global payment businesses merchant-level balance tracking, itemized fee breakdowns, and same-day exception flagging without a separate export or syncing step.